JUDICIAL FORECLOSURE

Judicial Foreclosure is the legal process by which a lender attempts to recover the amount owed on a defaulted loan by taking ownership of the mortgaged property and selling it. Typically, default is triggered when a borrower misses a specific number of monthly payments, but it can also happen when the borrower fails to meet other terms in the mortgage document.

Judicial Foreclosure can be a lengthy and complicated process, so it’s important to seek out professional help if you’re facing foreclosure. The law firm of LawInCabo can help you navigate the foreclosure process and protect your rights. We have extensive experience helping borrowers in Mexico keep their homes, and we can help you too.

The foreclosure process begins when a borrower defaults or misses at least one mortgage payment. The lender will then send a missed-payment notice that indicates that the month’s payment hasn’t been received. If the borrower doesn’t catch up on their payments within a certain period of time, the lender can foreclose on the property. There are two types of Foreclosures: judicial and non-judicial.

Judicial Foreclosure involve a court proceeding, while non-judicial Foreclosures do not. Mexico has its own Foreclosure process that is based on Mexican law. If you are facing Foreclosure in Mexico, it is important to seek legal counsel from a Mexican law firm that specializes in Foreclosure law.

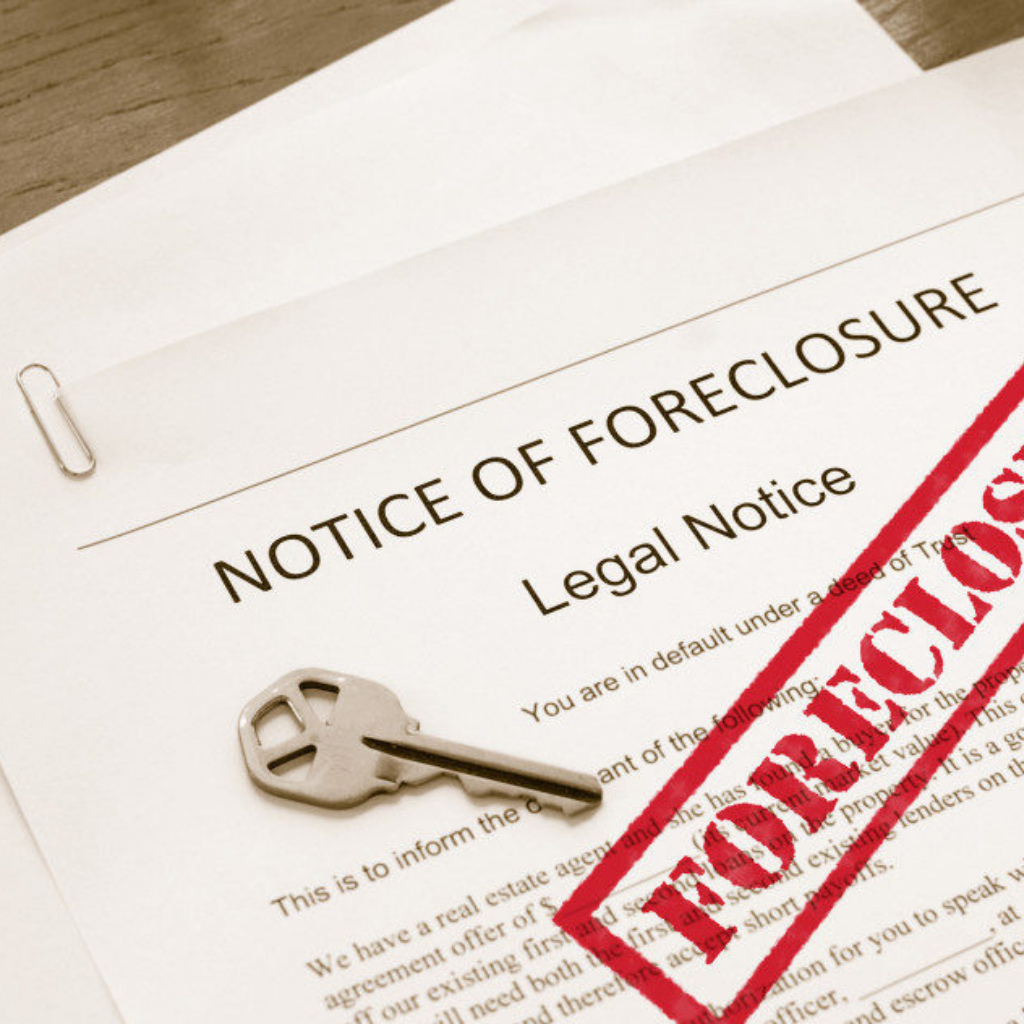

Defaulting on a mortgage can have significant consequences. The first step in the foreclosure process is typically a notice of foreclosure, which is a formal notice that indicates the borrower has failed to make a required mortgage payment. If the borrower does not remedy the situation within a certain period of time, the lender may begin the process of foreclosing on the property.

The judicial foreclosure process derives its legal basis from a mortgage or deed of trust contract, which gives the lender the right to use a property as collateral in case the borrower fails to uphold the terms of the mortgage document. Although the process varies by state, the foreclosure process generally begins when a borrower defaults or misses at least one mortgage payment. The lender then sends a missed-payment notice that indicates that the month’s payment hasn’t been received.

If the borrower doesn’t catch up on payments within a certain timeframe, usually 30 days, the lender can start judicial foreclosure proceedings. In judicial foreclosure proceedings, the lender files a lawsuit against the borrower to obtain the outstanding balance of the loan. Once the judicial foreclosure process is complete and the lender has obtained ownership of the property, it can sell the property through either a public auction or private sale. If you are facing foreclosure in Mexico, it is important to seek legal advice from a law firm specializing in Foreclosure law in Mexico.

In judicial foreclosure states, the lender initiates the foreclosure process by filing a lawsuit against the borrower. Once the lawsuit is filed, the court will issue a notice of default, which gives the borrower a certain amount of time to bring the mortgage current. If the borrower fails to do so, then the property will be scheduled for a foreclosure auction. In non-judicial foreclosure states, the lender does not need to go through the court system in order to foreclose on a property.

Instead, they can simply give the borrower a notice of default and then schedule the property for a foreclosure auction. If a property fails to sell at a foreclosure auction, or if it otherwise never went through one, then lenders—often banks—typically take ownership of the property and may add it to an accumulated portfolio of foreclosed properties, also called real estate owned. As a result, there are more delinquent loans and more foreclosures in judicial foreclosure states.